To approve a change to each Fund’s sub-classification under 1ELECTION OF DIRECTORS

SHAREHOLDERS OF ALL FUNDS VOTING TOGETHER

Background

The Board currently consists of seven Directors, five of whom are not “interested persons” (as that term is defined in Section 2(a)(19) of the Investment Company Act of 1940 (the “1940 Act”)) of the Company and VALIC (the “Independent Directors”). Dr. Judith L. Craven, Dr. Timothy J. Ebner and Dr. John E. Maupin, Jr. are Independent Directors who were previously elected to the Board by the Company’s shareholders on December 28, 2001. Thomas J. Brown and Yvonne M. Curl, both of whom are Independent Directors, have not been elected by shareholders and were elected by the Board as Directors on November 14, 2005, and November 1, 2020, respectively. Peter A. Harbeck is an “interested” Director under the 1940 Act due to his ownership of AIG stock and his prior relationships with VALIC and SunAmerica. Eric S. Levy is an “interested” Director under the 1940 Act due to his current affiliations with VALIC and AIG. Mr. Harbeck and Mr. Levy are referred to as “Interested Directors”. Mr. Harbeck was previously elected to the Board by the Company’s shareholders on December 28, 2001. Mr. Levy has not been elected by shareholders and was elected by the Board as a Director on May 1, 2017. Each Director serves on the Board until his or her successor is duly elected and qualified.

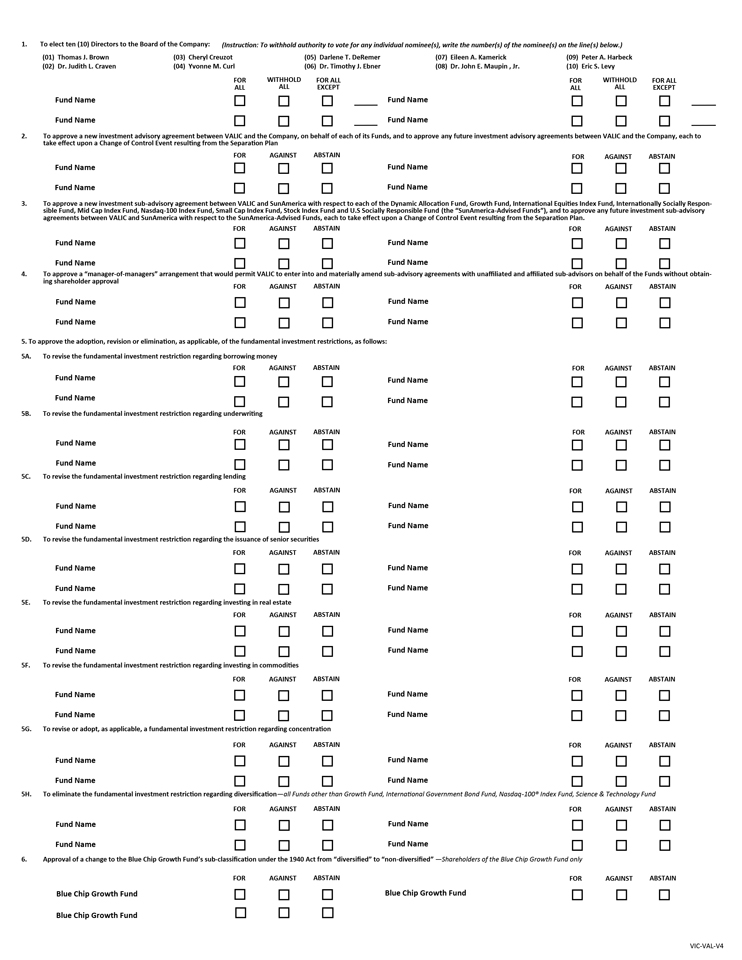

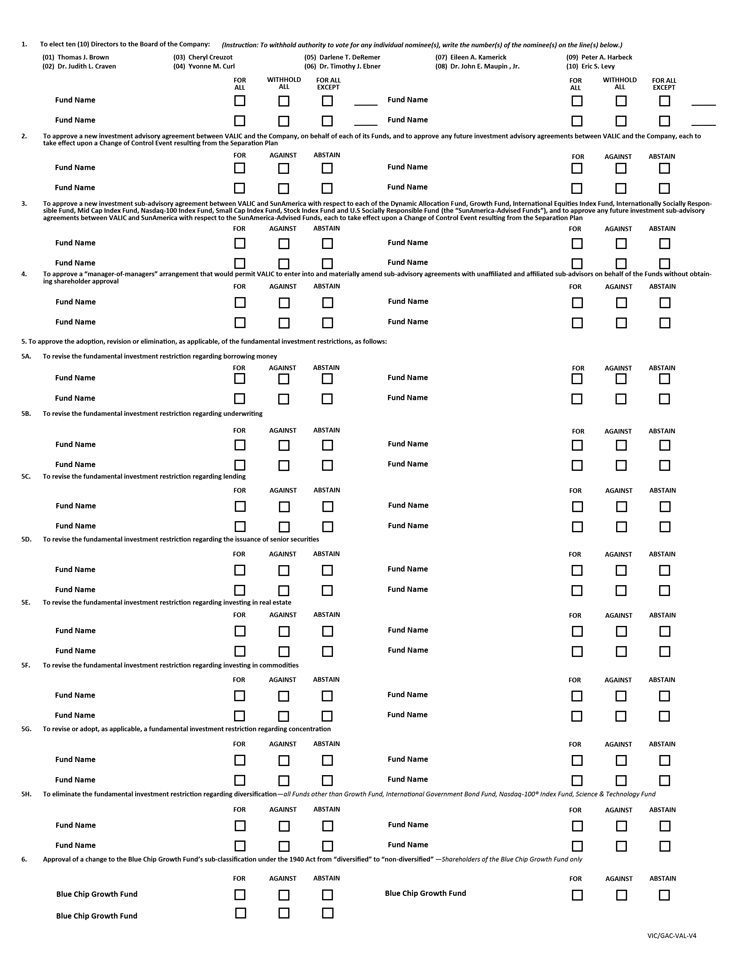

The Board has nominated each of the current Directors listed above for election to the Board. In addition, it has also approved an increase in the size of the Board to ten directors and nominated each of Cheryl Creuzot, Darlene T. DeRemer and Eileen A. Kamerick for election to the Board. The Board believes that the Company and the Funds’ shareholders would benefit from the expertise of Mses. Creuzot, DeRemer and Kamerick, who would be valuable additions to the Board and who would serve as Independent Directors if elected. Each nominee has consented to serving as a Director of the Company if elected and has also consented to being named in this Proxy Statement. If all nominees are elected, the Board would be comprised of ten Directors, eight of whom would be Independent Directors, each Director to hold office until his or her successor is elected and qualified.

The Board is asking shareholders of the Company to elect the ten nominees as Directors so that all members of the Board will have been elected by the shareholders. The 1940 Act requires that immediately after any vacancy on a registered investment company’s board of directors is filled (in a manner other than election by shareholders), at least two-thirds of the directors then holding office have been elected by the fund’s shareholders. The 1940 Act also provides that in the event that at any time less than a majority of the directors of a fund are elected by shareholders, a shareholder meeting must be held as promptly as possible for the purpose of electing directors to fill any vacancies. If all ten nominees are elected by shareholders at the Special Meeting, then in the event of any future vacancies, the remaining Directors may elect up to five additional Board members (assuming no subsequent changes to the composition of the Board).

In addition to the foregoing, in order to rely on certain exemptive rules promulgated by the Securities and Exchange Commission (the “SEC”), the Company must comply with certain requirements, including the requirement that a majority of the Directors on the Board be Independent Directors. The Board believes that it is in the best interests of the Company and the Funds’ shareholders to be able to rely on the exemptive rules. The Board also believes that good governance practices involve having a majority of its members be Independent Directors.

Information Regarding the Nominees

The following table lists the nominees for Director, their ages, current position(s) held with the Company, length of time served, principal occupations during the past five years, number of funds overseen

within the fund complex and other directorships/trusteeships held outside of the fund complex. Each nominee for Director was reviewed by the Governance Committee of the Board and nominated by the full Board. Dr. John E. Maupin, Jr. serves as the Chair of the Board. Unless otherwise noted, the address of each Director is 2929 Allen Parkway, Houston, Texas 77019. Information about the officers of the Company is provided in Exhibit A.

| | | | | | | | | | |

Name and Age | | Position(s) Held With Company(1) | | Term of Office and Length of Time Served | | Principal Occupation(s) During Past 5 Years | | Number of Funds in Fund Complex Overseen By Director

or Nominee

for

Director(2) | | Other Directorship(s) Held By Director or

Nominee for Director(3) |

| | | |

Independent Director Nominees | | | | | | |

| | | | | |

Thomas J. Brown Age: 76 | | Director | | 2005 – Present | | Retired. | | 36 | | Trustee, Virtus Funds (2011-2020). |

| | | | | |

Dr. Judith L. Craven Age: 76 | | Director | | 1998 – Present | | Retired. | | 36 | | Director, A.G. Belo Corporation, a media company (1992-2014); Director, SYSCO Corporation, a food marketing and distribution company (1996-2017); Director, Luby’s Inc. (1998-2019). |

| | | | | |

Cheryl Creuzot Age: 63 | | N/A | | N/A | | President and Chief Executive Officer of Wealth Development Strategies, LLC (2012-2019); President Emeritus, Wealth Development Strategies LLC (2019-Present). | | 36 | | Director, The Bancorp, Inc. – Audit and Risk Committees (2021-Present); Director, Amegy Bank (2021); Director, The Frenchy’s Companies (2013-Present); Commissioner, Port of Houston – Audit, Governance, Dredge Task Force and Community Relations Committees (2020 -Present); Executive Committee Member, MD Anderson University Cancer Foundation Board of Visitors (2010-Present); Director, Unity National Bank – Chair of Compliance, Audit, and Investment Committees (2008-2015). |

| | | | | | | | | | |

Name and Age | | Position(s) Held With Company(1) | | Term of Office and Length of Time Served | | Principal Occupation(s) During Past 5 Years | | Number of Funds in Fund Complex Overseen By Director

or Nominee

for

Director(2) | | Other Directorship(s) Held By Director or

Nominee for Director(3) |

Yvonne M. Curl Age: 67 | | Director | | 2020 – Present | | Retired. | | 36 | | Director, Encompass Health, provider of post-acute healthcare services (2004-Present); Director, Community Foundation of the Lowcountry (2018-Present); Director, Nationwide Insurance, insurance company (1998-2019); Director, Hilton Head Humane Association, animal shelter (2006-2019). |

| | | | | |

Darlene T. DeRemer Age: 66 | | N/A | | N/A | | Managing Partner, Grail Partners LLC (2005-2019). | | 36 | | Trustee, ARK ETF Trust (2014-Present); Trustee, Member of Investment and Endowment Committee of Syracuse University (2010-Present); Director, Alpha Healthcare Acquisition Corp. III (2021-Present); Interested Trustee, Esoterica Thematic Trust (2020-2021); Interested Trustee, American Independence Funds (2015-2019); Trustee, Risk X Investment Funds (2016-2020); Director, United Capital Financial Planners (2008-2019); Director, Hillcrest Asset Management (since 2007); Board Member, Confluence Technologies LLC (2018-2021). |

| | | | | | | | | | |

Name and Age | | Position(s) Held With Company(1) | | Term of Office and Length of Time Served | | Principal Occupation(s) During Past 5 Years | | Number of Funds in Fund Complex Overseen By Director

or Nominee

for

Director(2) | | Other Directorship(s) Held By Director or

Nominee for Director(3) |

Dr. Timothy J. Ebner Age: 73 | | Director | | 1998 – Present | | Professor and Head- Department of Neuroscience Medical School (1980-Present) and Pickworth Chair (2000-Present), University of Minnesota; Scientific Director, Society for Research on the Cerebellum (2008-Present); President, Association of Medical School Neuroscience Department Chairpersons (2011-2014). | | 36 | | Trustee, Minnesota Medical Foundation (2003-2013). |

| | | | | |

Eileen A. Kamerick Age: 64 | | N/A | | N/A | | Chief Executive Officer, The Governance Partners, LLC (consulting firm) (2015-Present); National Association of Corporate Directors Board Leadership Fellow (2016-Present, with Directorship Certification since 2019) and financial expert; Adjunct Professor, Georgetown University Law Center (2021-Present); Adjunct Professor, The University of Chicago Law School (2018-Present); formerly, Chief Financial Officer, Press Ganey | | 36 | | Director of the Legg Mason Closed-End Funds (2013-Present); Director of ACV Auctions Inc. (2021-Present); Director of Hochschild Mining plc (precious metals company) (2016-Present); Director of Associated Banc-Corp (financial services company) (2007-Present). |

| | | | | | | | | | |

Name and Age | | Position(s) Held With Company(1) | | Term of Office and Length of Time Served | | Principal Occupation(s) During Past 5 Years | | Number of Funds in Fund Complex Overseen By Director

or Nominee

for

Director(2) | | Other Directorship(s) Held By Director or

Nominee for Director(3) |

| | | | | | Associates (health care informatics company) (2012 to 2014); Managing Director and Chief Financial Officer, Houlihan Lokey (international investment bank) and President, Houlihan Lokey Foundation (2010 to 2012). | | | | |

| | | | | |

Dr. John E. Maupin, Jr. Age: 75 | | Director and Chair | | 1998 – Present | | Retired. President/CEO, Morehouse School of Medicine, Atlanta, Georgia (2006-2014). | | 36 | | Director, HealthSouth, Corporation, rehabilitation health care services (2004-Present); Director, Regions Financials Inc., bank holding company (2007-2019); Director, LifePoint Hospitals, Inc., hospital management (1999-2018) |

|

| Interested Director Nominee |

| | | | | |

Peter A. Harbeck(4) Harborside 5 185 Hudson Street Suite 3300 Jersey City, NJ 07311-4992 Age: 68 | | Director | | 2001 – Present | | Retired June 2019, formerly President (1995-2019), CEO (1997-2019) and Director (1992-2019), SunAmerica; Director, AIG Capital Services, Inc. (“ACS”) (1993-2019); Chairman, President and CEO, Advisor Group, Inc. (2004-2016). | | 36 | | None. |

| | | | | | | | | | |

Name and Age | | Position(s) Held With Company(1) | | Term of Office and Length of Time Served | | Principal Occupation(s) During Past 5 Years | | Number of Funds in Fund Complex Overseen By Director

or Nominee

for

Director(2) | | Other Directorship(s) Held By Director or

Nominee for Director(3) |

| | | | | |

Eric S. Levy(5) 2919 Allen Parkway Houston, TX 77019 Age: 57 | | Director | | 2017 – Present | | Executive Vice President, VALIC (2015-Present); Executive Vice President, Group Retirement, AIG (2015-Present); and Senior Vice President, Lincoln Financial Group (2010-2015). | | 36 | | None. |

| (1) | Directors serve until their successors are duly elected and qualified. |

| (2) | The term “Fund Complex” means two or more registered investment companies that (i) hold themselves out to investors as related companies for purposes of investment and investor services or (ii) have a common investment adviser or an investment adviser that is an affiliated person of the investment adviser of any of the other registered investment companies, VALIC. The Fund Complex includes the Company (36 funds), SunAmerica Series Trust (61 portfolios), and Seasons Series Trust (19 portfolios). |

| (3) | Directorships of companies required to report to the SEC under the Securities Exchange Act of 1934 (i.e., “public companies”) or other investment companies regulated under the 1940 Act, other than those listed under the preceding column. |

| (4) | Mr. Harbeck is considered to be an Interested Director because he owns shares of AIG, the ultimate parent of VALIC, and because of his prior relationships with VALIC and SunAmerica. Until his retirement on June 28, 2019, he served as President, CEO and Director of SunAmerica and Director of ACS. |

| (5) | Mr. Levy is considered to be an Interested Director because he serves as an officer of VALIC and AIG, VALIC’s ultimate parent company. |

Board’s Consideration of Each Nominee’s Qualifications, Experience, Attributes or Skills

The Board believes that the significance of each nominee’s experience, qualifications, attributes or skills is an individual matter (meaning that experience or knowledge that is important for one nominee may not have the same value for another) and that these factors are best evaluated at the Board level, with no single factor being a controlling factor. Among the attributes common to all nominees are their ability to review critically, evaluate, question and discuss information provided to them, to interact effectively with the other Directors (in the case of nominees who currently serve as Directors), VALIC, the sub-advisers, other service providers, legal counsel and the independent registered public accounting firm, and to exercise effective business judgment in the performance of their duties as Directors. The Board has also considered the contributions that each nominee can make to the Board and the Funds. A nominee’s ability to perform his or her duties effectively may have been attained through the nominee’s executive, business, consulting, public service and/or academic positions; experience from service as a Director of the Company (in the case of nominees who currently serve as Directors) and the other funds/portfolios in the Fund Complex (and/or in other capacities), other investment funds, public companies, or non-profit entities or other organizations; educational background or professional training; and/or other life experiences.

Additional information about each Director is set forth below, which supplements the information provided in the table above and describes some of the specific experiences, qualifications, attributes, or skills that each nominee possesses that the Board believes prepares them to be effective Directors.

Independent Directors

Thomas J. Brown. Mr. Brown has served as Director since 2005. Mr. Brown is also the chair of the Audit Committee and serves as the Audit Committee Financial Expert and as a member of each of the Brokerage, the Compliance and Ethics, and the Governance Committees. An “Audit Committee Financial Expert” is defined as a person who has the following attributes: (i) an understanding of generally accepted accounting principles and financial statements; (ii) the ability to assess the general application of such principles in connection with the accounting for estimates, accruals and reserves; (iii) experience preparing, auditing, analyzing or evaluating financial statements that present a breadth and level of complexity of accounting issues that are generally comparable to the breadth and complexity of issues that can reasonably be expected to be raised by the registrant’s financial statements, or experience actively supervising one or more persons engaged in such activities; (iv) an understanding of internal controls and procedures for financial reporting; and (v) an understanding of audit committee functions. Mr. Brown is a retired Chief Operating Officer and Chief Financial Officer of American General Asset Management, and previously was the Treasurer and CFO of the North American Funds. Mr. Brown also has substantial experience serving on boards of other mutual fund complexes.

Dr. Judith L. Craven. Dr. Craven has served as Director since 1998. Dr. Craven is also the chair of the Compliance and Ethics Committee and serves as a member of each of the Audit, the Brokerage, and the Governance Committees. Dr. Craven is a retired administrator, and has held numerous executive and directorship positions within the healthcare industry. Dr. Craven has substantial experience serving on local, state, and national boards, and is currently a director of Luby’s Restaurant and SYSCO Corporation, among other organizations.

Cheryl Creuzot. If elected to the Board, Ms. Creuzot is expected to serve as a member of each of the Audit, the Brokerage, the Compliance and Ethics, and the Governance Committees. Ms. Creuzot was formerly the President and Chief Executive Officer and Principal of Wealth Development Strategies, LLC and Wealth Development Investment Advisory, LLC, both Financial Industry Regulatory Authority and SEC regulated, financial advisory firms. Ms. Creuzot also has substantial experience serving on non-profit boards, and has significant securities and financial planning experience.

Yvonne M. Curl. Ms. Curl has served as Director since 2020. Ms. Curl is also the chair of the Brokerage Committee and serves as a member of each of the Audit, the Compliance and Ethics, and the Governance Committees. In addition, she has nearly 30 years of executive and business experience in various industries. Ms. Curl also has corporate governance experience serving on multiple public company and non-profit boards for nearly 30 years.

Darlene T. DeRemer. If elected to the Board, Ms. DeRemer is expected to serve as a member of each of the Audit, the Brokerage, the Compliance and Ethics, and the Governance Committees. Ms. DeRemer was formerly Managing Partner of Grail Partners, an advisory merchant bank serving the investment management industry. Prior to becoming an investment banker at Putnam Lovell NBF in 2003, Ms. DeRemer spent twenty-five years as a leading adviser to the financial services industry. Ms. DeRemer also has substantial experience serving on investment company boards and currently serves as Chair of ARK ETF Trust.

Dr. Timothy J. Ebner. Dr. Ebner has served as Director since 1998. Dr. Ebner is also the chair of the Governance Committee and serves as a member of each of the Audit, the Compliance and Ethics, and the Brokerage Committees. Dr. Ebner is Head of the Department of Neuroscience of the Medical School at the University of Minnesota. Dr. Ebner has experience serving on the boards of other mutual funds, as well as on the boards of several scientific foundations and non-profit organizations. Dr. Ebner is also an editor for the Journal of Neuroscience and is on the editorial board of three other neuroscience journals.

Eileen A. Kamerick. If elected to the Board, Ms. Kamerick is expected to serve as a member of each of the Audit, the Brokerage, the Compliance and Ethics, and the Governance Committees. Ms. Kamerick has

substantial experience in business and finance, including financial reporting, and experience as a board member of a highly regulated financial services company. Ms. Kamerick also has substantial experience serving on investment company boards and is currently a board member of the Legg Mason Closed End Funds, for which she serves as audit committee financial expert.

Dr. John E. Maupin, Jr. Dr. Maupin has served as Director since 1998. Dr. Maupin is the Chair of the Board and also serves as a member of each of the Audit, the Brokerage, the Compliance and Ethics, and the Governance Committees. Dr. Maupin is the retired President and Chief Executive Officer of Morehouse School of Medicine in Atlanta, Georgia, and has extensive executive and administrative experience at other organizations and companies within the healthcare industry. Dr. Maupin also currently serves on the boards of LifePoint Hospitals, Inc., HealthSouth Corporation, and Regions Financials, Inc.

Interested Directors

Peter A. Harbeck. Mr. Harbeck previously served as President, Chief Executive Officer and Director of SunAmerica and Director of ACS. As President and Chief Executive Officer, Mr. Harbeck was responsible for all of SunAmerica’s mutual fund businesses. During his over twenty-year tenure at SunAmerica, Mr. Harbeck held various positions, including Chief Operating Officer and Chief Administrative Officer. In addition, Mr. Harbeck has extensive experience on various fund and annuity boards.

Eric S. Levy. Mr. Levy has served as Director since May 1, 2017. Mr. Levy is Executive Vice President of VALIC and Executive Vice President, Group Retirement of AIG. Mr. Levy is also a Registered Principal for VALIC Financial Advisors, Inc., an affiliate of VALIC. Mr. Levy’s experience spans thirty-five years in financial services, including mutual funds, sub-advisory services, retirement services and insurance products at Fidelity, Allmerica Financial, Putnam Investments, Mercer and Lincoln Financial Group.

Leadership Structure and Oversight Responsibilities

Overall responsibility for oversight of the Company and its Funds rests with the Board. The Company, on behalf of the Funds, has engaged VALIC as the investment adviser which oversees the day-to-day operations of the Funds, and has engaged sub-advisers who manage the Funds’ assets on a day-to-day basis. VALIC has also engaged SunAmerica as the Funds’ administrator. The Board is responsible for overseeing VALIC, SunAmerica and the sub-advisers and any other service providers in the operations of the Funds in accordance with the provisions of the 1940 Act, applicable provisions of state and other laws, the Company’s charter and Bylaws, and each Fund’s investment objectives and strategies. The Board is presently composed of seven members, five of whom are Independent Directors. The Board currently conducts regular meetings at least quarterly and holds special in-person or telephonic meetings, or informal conference calls, to discuss specific matters that may arise or require action between regular Board meetings. The Independent Directors also meet at least quarterly in executive session, at which no Interested Director is present. The Independent Directors have engaged independent legal counsel to assist them in performing their oversight responsibilities.

The Board has appointed Dr. Maupin, an Independent Director, to serve as Chair of the Board. The Chair’s role is to preside at all meetings of the Board and to act as a liaison with service providers, including VALIC, SunAmerica, officers, attorneys, and other Directors generally, between meetings. The Chair may also perform such other functions as may be delegated by the Board from time to time. The Board has established four committees, i.e., Audit Committee, Governance Committee, Brokerage Committee and Compliance and Ethics Committee (each, a “Committee”) to assist the Board in the oversight and direction of the business and affairs of the Funds, and from time to time may establish informal working groups to review and address the policies and practices of the Funds with respect to certain specified matters. The Committee system facilitates the timely and efficient consideration of matters by the Directors, and facilitates effective oversight of compliance with legal and regulatory requirements and of the Funds’ activities and associated risks. The standing Committees currently conduct an annual review of their charters, which includes a review of their responsibilities

and operations. The Governance Committee and the Board as a whole also conduct an annual evaluation of the performance of the Board, including consideration of the effectiveness of the Board’s committee structure. The Board has determined that the Board’s leadership structure is appropriate because it allows the Board to exercise informed and independent judgment over the matters under its purview and it allocates areas of responsibility among the Committees and the full Board in a manner that enhances efficient and effective oversight.

The Funds are subject to a number of risks, including, among others, investment, compliance, operational, regulatory and valuation risks. Risk oversight forms part of the Board’s general oversight of the Funds and is addressed as part of various Board and Committee activities. Day-to-day risk management functions are subsumed within the responsibilities of VALIC and SunAmerica, who carry out the Funds’ investment management and business affairs, and also by the Funds’ sub-advisers and other service providers in connection with the services they provide to the Funds. Each of VALIC, SunAmerica, the sub-advisers and other service providers have their own independent interest in risk management, and their policies and methods of risk management will depend on their functions and business models. As part of its regular oversight of the Funds, the Board, directly and/or through a Committee, interacts with and reviews reports from, among others, VALIC, SunAmerica, the sub-advisers and the Funds’ other service providers (including the Funds’ distributor and transfer agent), the Funds’ Chief Compliance Officer, the independent registered public accounting firm for the Funds, legal counsel to the Funds, and internal auditors for SunAmerica or its affiliates, as appropriate, relating to the operations of the Funds. The Board recognizes that it may not be possible to identify all of the risks that may affect each Fund or to develop processes and controls to eliminate or mitigate their occurrence or effects. The Board may, at any time and in its discretion, change the manner in which it conducts risk oversight.

Effective January 1, 2022, Independent Directors receive an annual retainer of $263,000 (Chair receives an additional $57,750 retainer). The Independent Directors receive a fee of $4,000 for additional special meetings ($13,125 if it is determined a full meeting fee is appropriate). The Audit Committee chair, also the Audit Committee Financial Expert, receives a retainer of $38,500. The Governance Committee chair receives a retainer of $26,000, the Compliance and Ethics Committee chair receives a retainer of $15,000, and the Brokerage Committee chair receives a retainer of $15,000.

The Audit Committee is comprised of all Independent Directors, with Mr. Brown as chair and Mr. Brown serving as the “Audit Committee Financial Expert.” The Audit Committee recommends to the Board the selection of independent registered public accounting firm for the Funds and reviews with such independent accounting firm the scope and results of the annual audit, reviews the performance of the accounts, and considers any comments of the independent accounting firm regarding the Funds’ financial statements or books of account. The Audit Committee has a Sub-Committee to approve audit and non-audit services and it is comprised of Mr. Brown, Dr. Ebner and Dr. Maupin. The Board has adopted an Audit Committee charter, a copy of which is found in Exhibit B. During the fiscal year ended May 31, 2022, the Audit Committee held four (4) meetings.

The Governance Committee is comprised of all Independent Directors, with Dr. Ebner as chair. The Governance Committee recommends to the Board nominees for Independent Director membership, reviews governance procedures and Board composition, and periodically reviews Director compensation. The Funds do not have a standing compensation committee. The Board has adopted a Governance Committee charter, a copy of which is found in Exhibit C. During the fiscal year ended May 31, 2022, the Governance Committee held six (6) meetings.

The Brokerage Committee is comprised of all Independent Directors, with Ms. Curl as chair. The Brokerage Committee reviews brokerage issues but does not meet on a formal basis. During the fiscal year ended May 31, 2022, the Brokerage Committee held three (3) meetings.

The Compliance and Ethics Committee is comprised of all Independent Directors, with Dr. Craven as chair. The Compliance and Ethics Committee addresses issues that arise under the Code of Ethics for the Principal Executive and Principal Accounting Officers as well as any material compliance matters arising under

Rule 38a-1 policies and procedures as approved by the Board. During the fiscal year ended May 31, 2022, the Compliance and Ethics Committee held one (1) meeting.

The Independent Directors are reimbursed for certain out-of-pocket expenses by the Company.

Compensation of Independent Directors

The following table sets forth the aggregate compensation paid to each Independent Director by the Company for his/her service as Director during the most recently completed fiscal year and by the Company and/or other registered investment companies in the Fund Complex for the most recently completed calendar year. Interested Directors are not eligible for compensation or retirement benefits and thus, are not shown below.

| | | | | | | | |

Name of Director1 | | Aggregate

Compensation

from

Company | | | Total

Compensation

From Fund

Complex

Paid to

Directors2 | |

Mr. Thomas J. Brown | | $ | 305,375 | | | $ | 305,375 | |

Dr. Judith L. Craven | | $ | 281,875 | | | $ | 343,999 | |

Ms. Yvonne M. Curl | | $ | 266,875 | | | $ | 266,875 | |

Dr. Timothy Ebner3 | | $ | 260,700 | | | $ | 260,700 | |

Dr. John E. Maupin, Jr. | | $ | 324,625 | | | $ | 324,625 | |

| 1 | Directors receive no pension or retirement benefits from the Company or any other funds in the Fund Complex. |

| 2 | Includes the Company, VALIC Company II, SunAmerica Senior Floating Rate Fund, Inc., SunAmerica Income Funds, SunAmerica Equity Funds, SunAmerica Series, Inc., SunAmerica Specialty Series, SunAmerica Money Market Funds, Inc. and Anchor Series Trust. |

| 3 | Dr. Ebner previously deferred a portion of compensation under the Deferred Compensation Plan discussed below. As of May 31, 2022, the current value of the deferred compensation is $862,903. |

The Board has approved a Deferred Compensation Plan (the “Deferred Plan”) for its Independent Directors who are not officers, directors, or employees of VALIC or an affiliate of VALIC. The purpose of the Deferred Plan is to permit such Independent Directors to elect to defer receipt of all or some portion of the fees payable to them for their services to the Company, therefore allowing postponement of taxation of income and tax-deferred growth on the earnings. Under the Deferred Plan, an Independent Director may make an annual election to defer all or a portion of his/her future compensation from the Company.

The Company’s retirement policy provides that each Independent Director shall retire from service as an Independent Director at the end of the calendar year in which he or she turns 75 years of age, except that for an Independent Director whose term of service began prior to January 1, 2016, such Independent Director may request an additional year of eligibility as an Independent Director subject to approval by the other Independent Directors up to a maximum of five additional years (to age 80).

Director Ownership of Fund Shares

The following table shows the dollar range of shares beneficially owned by the Director nominees that they are nominated to oversee as of [ ], 2022.

| | | | | | | | |

Name of Director | | Dollar

Range of

Equity

Securities

in the

Company | | | Aggregate

Dollar

Range

of Equity

Securities

in All

Registered

Investment

Companies

Overseen

by

Director in

Family(1) | |

Independent Directors/Nominees: | | | | | | | | |

Mr. Thomas J. Brown | | $ | [ | ] | | $ | [ | ] |

Dr. Judith L. Craven | | | [ | ] | | | [ | ] |

Ms. Cheryl Creuzot | | | [ | ] | | | [ | ] |

Ms. Yvonne M. Curl | | | [ | ] | | | [ | ] |

Ms. Darlene T. DeRemer | | | [ | ] | | | [ | ] |

Dr. Timothy Ebner | | | [ | ] | | | [ | ] |

Ms. Eileen A. Kamerick | | | [ | ] | | | [ | ] |

Dr. John E. Maupin, Jr. | | | [ | ] | | | [ | ] |

Interested Director/Nominee: | | | | | | | | |

Mr. Peter A. Harbeck | | $ | [ | ] | | $ | [ | ] |

Mr. Eric S. Levy | | | [ | ] | | | [ | ] |

| (1) | Includes the Company (36 series). |

As of [ ], 2022, the Directors and officers of the Company owned in the aggregate less than 1% of the total outstanding shares of each Fund which they oversee (or are nominated to oversee).

As of [ ], 2022, no Independent Directors nor any of their immediate family members owned beneficially or of record any securities in VALIC, any sub-adviser or the distributor or any person other than a registered investment company, directly or indirectly, controlling, controlled by or under common control with such entities.

Shareholder Communications with the Board

Shareholders wishing to communicate with members of the Board may submit a written communication to the Board of Directors, c/o the Secretary of VALIC Company I at 2929 Allen Parkway, Houston, Texas 77019.

Other Board-Related Matters

During the Company’s fiscal year ended May 31, 2022, the Board held six (6) meetings (including regularly scheduled and special meetings), and each Director proposed for election at the Special Meeting who currently serves on the Board attended at least 75% of the meetings of the Board and all committees of which he or she was a member.

Fees Paid to Independent Registered Public Accounting Firm

PricewaterhouseCoopers LLP (“PwC”) serves as the independent registered public accounting firm for the Funds. In addition, PwC prepares each Fund’s federal and state annual income tax returns and provides

certain non-audit services. The Audit Committee has selected PwC as the Funds’ independent registered public accounting firm for the current fiscal year and such selection has been ratified by the Board. Representatives of PwC are not expected to be present at the Special Meeting, but have been given the opportunity to make a statement if they so desire and will be available should any matter arise requiring their presence. PwC has informed the Company that it has no material direct or indirect financial interest in any Fund.

The table below sets forth the aggregate fees billed by PwC for each Fund’s most recent two fiscal years for (1) professional services rendered for audit services, including the audit or review of each Fund’s financial statements and services normally provided in connection with statutory and regulatory filings or engagements for those fiscal years; (2) audit-related services reasonably related to the audit or review of each Fund’s financial statements not reported under (1); (3) professional services rendered for tax compliance, tax advice, and tax planning; and (4) other products and services not reported under (1) through (3).

| | | | | | | | | | | | | | | | | | | | |

Fund | | Fiscal

Year | | | Audit

Services | | | Audit-

Related

Services | | | Tax

Services | | | Other

Services | |

Aggressive Growth Lifestyle Fund | | | 2022 | | | $ | 24,365 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,655 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Asset Allocation Fund | | | 2022 | | | $ | 36,214 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,160 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Blue Chip Growth Fund | | | 2022 | | | $ | 24,594 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,878 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Capital Appreciation Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Conservative Growth Lifestyle Fund | | | 2022 | | | $ | 24,365 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,655 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Core Bond Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Dividend Value Fund | | | 2022 | | | $ | 24,594 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,878 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Dynamic Allocation Fund | | | 2022 | | | $ | 25,279 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 24,543 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Emerging Economies Fund | | | 2022 | | | $ | 35,897 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 34,851 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Global Real Estate Fund | | | 2022 | | | $ | 25,939 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,183 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Global Strategy Fund | | | 2022 | | | $ | 38,326 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 37,210 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Government Securities Fund | | | 2022 | | | $ | 30,926 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 30,025 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Growth Fund | | | 2022 | | | $ | 24,593 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,877 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

High Yield Bond Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Inflation Protected Fund | | | 2022 | | | $ | 32,975 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 32,014 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

International Equities Index Fund | | | 2022 | | | $ | 35,897 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 34,851 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

International Government Bond Fund | | | 2022 | | | $ | 36,576 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,511 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

International Growth Fund | | | 2022 | | | $ | 34,147 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 33,152 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

International Opportunities Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | | | | | | | | | | | | | | | | | | |

Fund | | Fiscal

Year | | | Audit

Services | | | Audit-

Related

Services | | | Tax

Services | | | Other

Services | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

International Socially Responsible Fund | | | 2022 | | | $ | 26,344 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,577 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

International Value Fund | | | 2022 | | | $ | 34,147 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 33,152 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Large Capital Growth Fund | | | 2022 | | | $ | 24,592 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,876 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Mid Cap Index Fund | | | 2022 | | | $ | 26,342 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,575 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Mid Cap Strategic Growth Fund | | | 2022 | | | $ | 24,593 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,877 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Mid Cap Value Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Moderate Growth Lifestyle Fund | | | 2022 | | | $ | 24,365 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,655 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Nasdaq-100® Index Fund | | | 2022 | | | $ | 26,343 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,576 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Science & Technology Fund | | | 2022 | | | $ | 24,593 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,877 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Small Cap Growth Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Small Cap Index Fund | | | 2022 | | | $ | 26,342 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,575 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Small Cap Special Values Fund | | | 2022 | | | $ | 24,592 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,876 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Small Cap Value Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Stock Index Fund | | | 2022 | | | $ | 26,342 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,575 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Systematic Core Fund | | | 2022 | | | $ | 26,344 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 25,577 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

Systematic Value Fund | | | 2022 | | | $ | 24,594 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 23,878 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

U.S. Socially Responsible Fund | | | 2022 | | | $ | 36,550 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

| | | 2021 | | | $ | 35,485 | | | $ | 0 | | | $ | 0 | | | $ | 0 | |

There were no fees for audit-related services, tax services or other services approved by the Audit Committee pursuant to Rule 2-01(c)(7)(i)(C) of Regulation S-X for the 2021 or 2022 fiscal years. Fees for audit-related services, tax services or other services required to be approved by the Audit Committee pursuant to Rule 2-01(c)(7)(ii) of Regulation S-X for the 2021 or 2022 fiscal years were $610,825 and $403,601, respectively.

There were no fees billed by PwC to VALIC or any entity controlling, controlled by, or under common control with VALIC (the “VALIC Affiliates”) for the 2021 or 2022 fiscal years that are required by Rule 2-01(c)(7)(i) to be pre-approved by the Audit Committee.

The Audit Committee pre-approves all audit services provided by PwC to the Company and approves all non-audit services provided by PwC to the Company, VALIC, and VALIC Affiliates, if an engagement by VALIC or a VALIC Affiliate relates directly to the operations and financial reporting of the Company. The Audit Committee has not established any pre-approval policies and procedures that permit the pre-approval of the

above services other than by the full Audit Committee. Certain de minimis exceptions are permitted for non-audit services in accordance with Rule 2-01(c)(7)(i)(C) of Regulation S-X.

No fees billed to the Company, VALIC or VALIC Affiliates for audit-related services, tax services, or other services were approved pursuant to Rule 2-01(c)(7)(i)(C) of Regulation S-X.

PwC billed aggregate fees for non-audit services rendered to the Company, VALIC, and VALIC Affiliates that provide ongoing services to the Company of $849,920 for the 2021 fiscal year and $403,601 for the 2022 fiscal year. The Audit Committee was not required to consider whether non-audit services provided by PwC to VALIC, or to VALIC Affiliates that provide ongoing services to the Company, that were notpre-approved pursuant to Rule 2-01(c)(7)(ii) of Regulation S-X, were compatible with maintaining PwC’s independence.

THE BOARD UNANIMOUSLY RECOMMENDS THAT YOU VOTE “FOR” THE ELECTION OF EACH NOMINEE TO THE BOARD.

PROPOSAL 2

APPROVAL OF INVESTMENT ADVISORY AGREEMENTS

SHAREHOLDERS OF THE FUNDS VOTING SEPARATELY WITH RESPECT TO THEIR FUND

Background

As required by the 1940 Act, the Company’s current investment advisory agreement with VALIC automatically terminates in the event of an assignment, which includes a direct or indirect transfer of a controlling block of the voting securities of VALIC. This provision effectively requires a Fund’s shareholders to vote on a new investment advisory agreement if VALIC experiences a transfer of a controlling block of its voting securities for purposes of the 1940 Act.

As discussed above, it is anticipated that one or more of the transactions contemplated by the Separation Plan could be deemed a Change of Control Event resulting in the automatic termination of VALIC’s existing investment advisory agreement (the “Current Advisory Agreement”) and investment sub-advisory agreements, although Corebridge’s initial public offering is not anticipated to result in a Change of Control Event. In order to ensure that the existing investment advisory and sub-advisory services can continue uninterrupted, the Board has approved a new investment advisory agreement with VALIC in connection with the Separation Plan. Shareholders are being asked to approve the new investment advisory agreement with VALIC, the Funds’ current investment adviser, (the “Proposed Agreement”), which would be effective after the first Change of Control Event that occurs after shareholder approval. As part of Proposal 2, shareholders are also voting to approve any future advisory agreements with VALIC (the “Future Agreements” and together with the Proposed Agreement, the “New Advisory Agreements”) if there are subsequent Change of Control Events arising from completion of the Separation Plan that terminate the Proposed Agreement after the first Change of Control Event.

If there is a change from the facts described in this Proxy Statement that is material to shareholders of the Funds in the context of a vote on an advisory agreement, any shareholder approval received at the Special Meeting would no longer be valid to approve Future Agreements that would otherwise be approved in the event of subsequent Change of Control Events. This judgment will be made by VALIC in consultation with counsel to the Company and reviewed by the Board. If an investment advisory agreement were to terminate without valid shareholder approval, the Board and the shareholders of each Fund may be asked to approve new investment advisory agreements to permit VALIC to continue to provide services to the Funds.

Information about VALIC

VALIC is located at 2929 Allen Parkway, Houston, Texas 77019. VALIC serves as investment adviser for all of the Funds. As investment adviser, VALIC oversees the day-to-day operations of each Fund and supervises the purchase and sale of Fund investments. VALIC employs investment sub-advisers that make investment decisions for the Funds. VALIC is a Texas corporation, and managed or advised assets in excess of $28 billion as of June 30, 2022. VALIC is an indirect, majority-owned subsidiary of American General Life Insurance Company (“AGL”). AGL is a stock life insurance company organized under the laws of the state of Texas and is located at 2727-A Allen Parkway, Houston, Texas 77019. It is an indirect, wholly-owned subsidiary of Corebridge. Corebridge is currently a direct, majority-owned subsidiary of AIG and is located at 21650 Oxnard Street, Suite 750, Woodland Hills, California 91367.

The following table lists the names and principal occupations of VALIC’s principal executive officers and directors. The business address of each person listed below is 2929 Allen Parkway, Houston, Texas 77019.

| | |

Name | | Principal Occupation |

Roger A. Craig | | Senior Vice President, General Counsel and Assistant Secretary |

Emily W. Gingrich | | Director, Senior Vice President, Chief Actuary and Corporate Illustration Actuary |

Elias F. Habayeb | | Director, Executive Vice President and Chief Financial Officer |

Kevin T. Hogan | | Chairman of the Board, Chief Executive Officer and President |

Gilliane E. Isabelle | | Director, Senior Vice President and Chief Distribution Officer |

Kyle L. Jennings | | Senior Vice President and Chief Compliance Officer |

Todd A. McGrath | | Executive Vice President and Chief Operating Officer |

Jonathan J. Novak | | Chief Executive Officer, Institutional Markets |

Sabra R. Purtill | | Director, Senior Vice President and Chief Investment Officer |

Sabyasachi Ray | | Director and Senior Vice President |

Robert J. Scheinerman | | Director and Chief Executive Officer, Group Retirement |

Description of the New Advisory Agreements

The description of the Proposed Agreement that follows is qualified entirely by reference to the form of Proposed Agreement included in Exhibit D to this Proxy Statement. (As indicated below, the advisory fee rate for each Fund is provided in Exhibit E.) For purposes of this subsection, references to the Proposed Agreement include the Future Agreement. The Proposed Agreement is substantially identical in all material respects to the Current Advisory Agreement, except for new effective and termination dates, an updated list of Funds, the addition of language regarding VALIC’s payment due date and proration, and the addition of notices and counterparts provisions. The Proposed Agreement would become effective after the first Change of Control Event resulting from the Separation Plan that occurs after shareholder approval, and each Future Agreement would become effective upon a subsequent Change of Control Event resulting from the Separation Plan. The material terms of the Proposed Agreement are discussed in more detail below.

Services

No changes to the services provided by VALIC as specified under the Current Advisory Agreement are proposed in connection with Proposal 2.

Both the Current Advisory Agreement and the Proposed Agreement provide that VALIC shall, subject to the control, direction, and supervision of the Board and in conformity with all applicable laws and regulations, the Company’s organizational documents and its registration statement, (a) manage the investment and reinvestment of the assets of the Funds including, for example, the evaluation of pertinent economic, statistical, financial, and other data, the determination of the industries and companies to be represented in each Fund’s portfolio, and the formulation and implementation of investment programs; (b) maintain a trading desk and place all orders for the purchase and sale of portfolio investments for each Fund’s account with brokers or dealers selected by VALIC, or arrange for any other entity to provide a trading desk and to place orders with brokers and dealers selected by VALIC, subject to VALIC’s control, direction, and supervision; and (c) furnish to the Funds office space, facilities, equipment and personnel adequate to provide the services described above and pay the compensation to the Company’s Directors and officers who are interested persons of VALIC.

Appointment of Sub-advisers

No changes to the authority of VALIC to appoint sub-advisers are proposed in connection with Proposal 2.

Both the Current Advisory Agreement and the Proposed Agreement permit VALIC to employ a sub-adviser for each of its Funds for the purpose of providing investment management services with respect to the Fund, provided that (a) the compensation to be paid to such sub-adviser shall be the sole responsibility of VALIC, (b) the duties and responsibilities of the sub-adviser shall be as set forth in a sub-advisory agreement including VALIC and the sub-adviser as parties, (c) such sub-advisory agreement shall be adopted and approved in conformity with applicable laws and regulations, and (d) such sub-advisory agreement may be terminated at any time, on not more than 60 days’ written notice.

VALIC and the Company may rely on an exemptive order from the SEC that permits VALIC to enter into and materially amend sub-advisory agreements with unaffiliated sub-advisers without obtaining shareholder approval (the “VALIC Order”). The VALIC Order applies to the Company and its Funds, and is subject to certain conditions, including the requirement that the Board, including a majority of Independent Directors, approve any new sub-advisory agreement or material amendment to a sub-advisory agreement and that VALIC send shareholders an information statement complying with the conditions of Regulation 14C under the Securities Exchange Act of 1934, as amended, within 90 days after the retention of a new sub-adviser or a material amendment to an existing sub-advisory agreement.

As with the Current Advisory Agreement, the current sub-advisory agreements between VALIC and any sub-advisers with respect to a Fund will automatically terminate upon any Change of Control Event. VALIC and the Company expect to rely on the VALIC Order to enter into new sub-advisory agreements with the current, unaffiliated sub-advisers to the Funds.

Expenses

No changes to the expenses provisions of the Current Advisory Agreement are proposed in connection with Proposal 2.

Both the Current Advisory Agreement and the Proposed Agreement provide that VALIC shall bear the expense of discharging its responsibilities under the Agreement and the Company shall pay, or arrange for others to pay, all its expenses other than those which the Agreement expressly states are payable by VALIC. Expenses payable by the Company include, but are not limited to (i) interest and taxes; (ii) brokerage commissions and other expenses of purchasing and selling portfolio investments; (iii) compensation of its Directors and officers other than those persons who are interested persons of VALIC; (iv) fees of outside counsel to and of independent auditors of the Company selected by the Board; (v) fees for accounting services; (vi) custodial, registration, and transfer agency fees; (vii) expenses related to the repurchase or redemption of its shares including expenses related to a program of periodic repurchases or redemptions; (viii) expenses related to issuance of its shares against payment therefor by, or on behalf of, the subscribers thereto; (ix) fees and related expenses of registering and qualifying the Company and its shares for distribution under state and federal securities laws; (x) expenses of printing and mailing to existing shareholders of registration statements, prospectuses, reports, notices and proxy solicitation materials of the Company; (xi) all other expenses incidental to holding meetings of the Company’s shareholders including proxy solicitations therefor; (xii) expenses for servicing shareholder accounts; (xiii) insurance premiums for fidelity coverage and errors and omissions insurance; (xiv) dues for the Company’s membership in trade associations approved by the Board; and (xv) such non-recurring expenses as may arise, including those associated with actions, suits, or proceedings to which the Company is a party and the legal obligation which the Company may have to indemnify its officers, Directors and employees with respect thereto. The Company shall allocate the foregoing expenses among the Funds.

Contractual Advisory Fees

No changes in the contractual advisory fees for the Funds are proposed in connection with Proposal 2. Exhibit E includes the fee schedules for each Fund. Exhibit F provides information on the compensation paid to VALIC by each registered investment company with an investment objective similar to the investment objectives of the Funds.

Liability

No changes to the liability provisions of the Current Advisory Agreement are proposed in connection with Proposal 2.

Both the Current Advisory Agreement and the Proposed Agreement provide that VALIC shall not be liable to the Company, or to any shareholder of the Company, for any act or omission in rendering services under the Agreements, or for any losses sustained in the purchase, holding, or sale of any portfolio security, so long as there has been no willful misfeasance, bad faith, negligence, or reckless disregard of obligations or duties on the part of VALIC.

Term and Continuance

No changes to the term and continuance provisions of the Current Advisory Agreement are proposed in connection with Proposal 2. The Current Advisory Agreement and the Proposed Agreement would differ only to the extent of their effective and termination dates.

If approved by shareholders, the Proposed Agreement will be effective after the first Change of Control Event resulting from the Separation Plan that occurs after shareholder approval or any subsequent Change of Control Event resulting from the Separation Plan in the case of a Future Agreement. After an initial two-year term, the Proposed Agreement would continue in effect only so long as such continuance is approved at least annually by the vote of a majority of the Company’s Directors who are not parties to the Agreement or interested persons of any such parties, cast in person at a meeting called for the purpose of voting on such approval, and by a vote a majority of the Company’s Board or a majority of a Fund’s outstanding voting securities.

Termination

No changes to the termination provisions of the Current Advisory Agreement are proposed in connection with Proposal 2.

Both the Current Advisory Agreement and the Proposed Agreement provide that the Agreement may be terminated at any time as to a Fund, without payment of any penalty, as to any Fund at any time by the Company’s Board or by the vote of a majority of that Fund’s outstanding voting securities on 30-60 days’ prior written notice to VALIC, or by VALIC, on not more than 60 days’ nor less than 30 days’ written notice, or upon such shorter notice as may be mutually agreed upon. The Agreement automatically terminates in the event of its assignment.

For more information on when the Current Advisory Agreement was last approved by shareholders, see Exhibit E.

Factors Considered by the Board

At various meetings over the prior year, the Board discussed the Separation Plan with VALIC and certain AIG representatives. The Board was informed that in connection with the Separation Plan, Corebridge and AIG entered into agreements to effectuate, through a series of steps, a contribution of substantially all of the

entities that conduct AIG’s investment management operations, including VALIC and SunAmerica, from AIG to Corebridge. The Board understands that it is anticipated that one or more of the transactions contemplated by the Separation Plan could be deemed a Change of Control Event resulting in the automatic termination of the Current Advisory Agreement and Current Sub-Advisory Agreements (the “Current Advisory Contracts”) and that in order to ensure that the existing investment advisory and sub-advisory services can continue uninterrupted, the Board would need to approve a new investment advisory agreement with VALIC, as well as new sub-advisory agreements with the existing sub-advisers to certain Funds, in connection with the Separation Plan. Shareholders of each Fund will be asked to approve the New Advisory Agreements and shareholders of the SunAmerica Sub-Advised Funds will be asked to approve the New Sub-Advisory Agreements between VALIC and SunAmerica. Shareholder approval of new sub-advisory agreements with the current, unaffiliated sub-advisers to the Funds is not required due to the Funds’ current exemptive order that permits VALIC, subject to the approval of the Board, but without the need for shareholder approval, to enter into and materially amend sub-advisory agreements with unaffiliated sub-advisers.

At meetings held on August 2-3, 2022, the Board, including the Independent Directors, unanimously approved with respect to all of the Funds, the Proposed Agreement, the New SunAmerica Sub-Advisory Agreement and the new sub-advisory agreements between VALIC and each of the following sub-advisers of the Funds (collectively, the “New Advisory Contracts”): AllianceBernstein L.P. Allspring Global Investments, LLC, BlackRock Investment Management, LLC, Boston Partners Global Investors, Inc., Brandywine Global Investment Management, LLC, ClearBridge Investments, LLC, Columbia Management Investment Advisers, LLC, Delaware Investments Fund Advisers, Franklin Advisers, Inc., Goldman Sachs Asset Management, L.P., Invesco Advisers, Inc., Invesco Asset Management Limited, J.P. Morgan Investment Management Inc., Janus Capital Management, LLC, Macquarie Investment Management Global Limited, Macquarie Funds Management Hong Kong Limited, Massachusetts Financial Services Company, Morgan Stanley Investment Management Company, Morgan Stanley Investment Management Inc., PineBridge Investments LLC, SunAmerica, T. Rowe Price Associates, Inc., T. Rowe Price Investment Management, Inc., Voya Investment Management Co. LLC and Wellington Management Company LLP (each a “Sub-Adviser,” and collectively, the “Sub-Advisers”).1 The Board also determined to recommend that shareholders of each Fund approve the New Advisory Agreements and shareholders of the SunAmerica Sub-Advised Funds approve the New Sub-Advisory Agreements.

At these meetings, which included meetings of the full Board and separate meetings of the Independent Directors, the Board considered, among other things, whether it would be in the best interests of each Fund and its respective shareholders to approve the New Advisory Contracts, and the anticipated impacts of the Separation Plan on each Fund and its shareholders. The Independent Directors met with representatives of VALIC to discuss the Separation Plan and the New Advisory Contracts. Throughout the process, the Independent Directors were assisted by their independent legal counsel and counsel to the Funds, who advised them on, among other things, their duties and obligations relating to their consideration of the New Advisory Contracts. The Independent Directors also met separately with their independent legal counsel to discuss the New Advisory Contracts outside of the presence of management.

Before or during the meetings, the Board sought additional information as it deemed necessary and appropriate. The Board’s evaluation of the New Advisory Contracts reflected the information provided specifically in connection with its review of the New Advisory Contracts, as well as, where relevant, information

| 1 | On March 25, 2020 and June 19, 2020, as a result of health and safety measures put in place to combat the global COVID-19 pandemic, the SEC issued exemptive orders (the “Orders”) pursuant to Sections 6(c) and 38(a) of the 1940 Act, that temporarily exempt registered investment management companies from the in-person voting requirements under the 1940 Act, subject to certain requirements, including that votes taken pursuant to the Orders are ratified at the next in-person meeting. The Board determined that reliance on the Orders was necessary or appropriate due to the circumstances related to current or potential effects of COVID-19 and therefore, the August 2-3, 2022 meeting was held by videoconference in reliance on the Orders. |

that was separately provided to the Board in connection with the most recent renewal of the Current Advisory Contracts at meetings held on July 11, 2022 and August 2-3, 2022 (the “2022 Contracts Review Meeting”) and at other Board meetings held throughout the prior year. The Board’s evaluation of the New Advisory Contracts also reflected the knowledge gained as Board members of the Funds with respect to services provided by VALIC, its affiliates, including SunAmerica, and each other Sub-Adviser to the Funds. In connection with their consideration of the New Advisory Contracts, the Independent Directors worked with their independent legal counsel to prepare requests for information that were submitted to VALIC. The Board’s requests for information sought information relevant to the Board’s consideration of the New Advisory Contracts, distribution arrangements, and other anticipated impacts of the Separation Plan on the Funds and their shareholders. VALIC provided documents and information in response to these requests for information. Representatives of senior management from VALIC participated in a portion of the meetings and addressed various questions from the Board.

The Board’s approvals and recommendations were based on its determination, within its reasonable business judgment, that it would be in the best interests of each Fund and its respective shareholders, for VALIC and, as applicable, the Sub-Advisers, to provide investment advisory, investment sub-advisory, and related services to the Funds, following the consummation of the Separation Plan.

In connection with the approval of the New Advisory Contracts, VALIC advised the Board about a variety of matters, including, but not limited to, the following:

The Current Advisory Contracts were last renewed by the Board, including all the Independent Directors, at the 2022 Contracts Review Meeting. In connection with that renewal, the Directors reviewed information regarding the nature, extent and quality of services provided by VALIC and each Sub-Adviser; the investment results of each Fund; the advisory fees paid to VALIC by the Funds and the sub-advisory fees paid to each Sub-Adviser by VALIC; VALIC’s and each Sub-Adviser’s costs in managing the Funds and their profitability from the Funds; and other benefits received by VALIC, each Sub-Adviser and their affiliates as a result of their relationship with the Funds.

The New Advisory Contracts are not expected to result in any changes to the nature, extent and quality of services provided by VALIC or any Sub-Adviser.

The personnel responsible for the management operations of the Funds, including each Company officer, are not expected to change as a result of the Separation Plan.

The New Advisory Contracts are not expected to result in any changes to the portfolio management of any Fund, including no changes to the Funds’ investment objectives, principal investment strategies or principal investment risks and the same portfolio managers are expected to continue to provide day-to-day management of the applicable Fund.

The New Advisory Contracts are not expected to result in any changes to the contractual investment advisory fees charged to the Funds.

The support expressed by the senior management of VALIC for the Separation Plan and VALIC’s recommendation that the Board approve the New Advisory Contracts.

That the Funds and VALIC or its affiliates will split the costs of the Special Meeting, including legal, audit, filing fees and other related expenses.

In addition to the matters noted above, in their deliberations regarding approval of the New Advisory Contracts, the Board considered the factors discussed below, among others.

Nature, Extent and Quality of Services.

The Board considered the benefits to shareholders of retaining VALIC and the Sub-Advisers and approving the New Advisory Contracts, particularly in light of the nature, extent, and quality of the services that have been provided by VALIC and the Sub-Advisers. The Board considered the services provided by VALIC and the Sub-Advisers in rendering investment management services to the Funds. The Board considered that VALIC is responsible for the management of the day-to-day operations of the Company, including but not limited to, general supervision of and coordination of the services provided by the Sub-Advisers, and is also responsible for monitoring and reviewing the activities of the Sub-Advisers and other third-party service providers. The Board also noted that VALIC’s and the Sub-Advisers’ management of the Company is subject to the oversight of the Board, and must be made in accordance with the investment objectives, policies and restrictions set forth in the Company’s prospectus and statement of additional information. The Board noted that VALIC monitors the performance of the Funds and from time-to-time recommends Sub-Adviser changes and/or other changes intended to improve the performance of the Funds. The Board considered the quality of the portfolio management services which have benefited and should continue to benefit each Fund and its shareholders, the organizational depth and resources of VALIC and each Sub-Adviser including the background and experience of VALIC’s and each Sub-Adviser’s management personnel, and the expertise of VALIC’s and each Sub-Adviser’s portfolio management team, as well as the investment methodology used by VALIC and each Sub-Adviser.

The Board noted that VALIC personnel meet on a regular basis to discuss the performance of the Company, as well as the positioning of the insurance products, employer-sponsored retirement plans and the Funds generally vis-à-vis competitors. The Board also considered VALIC’s financial condition and whether it continues to have the financial wherewithal to provide the services under the New Advisory Agreement with respect to each Fund. The Board also considered VALIC’s risk management processes. The Board further considered the significant risks assumed by VALIC in connection with the services provided to the Funds, including entrepreneurial risk in sponsoring new Funds and ongoing risks such as operational, reputational, liquidity, litigation, regulatory and compliance risks with respect to all Funds.

With respect to the services provided by the Sub-Advisers, the Board considered information provided to the Board regarding the services provided by each Sub-Adviser, including information presented throughout the previous year and at the 2022 Contracts Review Meeting. The Board noted that each Sub-Adviser (i) determines the securities to be purchased or sold on behalf of the Fund(s) it manages as may be necessary in connection therewith; (ii) provides VALIC with records concerning its activities, which VALIC or the Funds are required to maintain; and (iii) renders regular reports to VALIC and to officers and Directors of the Funds concerning its discharge of the foregoing responsibilities. The Board reviewed each Sub-Adviser’s history and investment experience as well as information regarding the qualifications, background and responsibilities of the Sub-Adviser’s investment, compliance and other personnel who provide services to the Funds. The Board also took into account the financial condition of each Sub-Adviser. The Board also considered each Sub-Adviser’s brokerage practices and risk management processes.

The Board reviewed VALIC’s and SunAmerica’s compliance program and personnel. The Board also considered the performance of certain portions of the business continuity plan which have been invoked in response to the COVID-19 pandemic. The Board noted that SunAmerica is an affiliated company of VALIC and serves as the administrator to the Funds, as well as sub-advises certain Funds. The Board also considered VALIC’s and each Sub-Adviser’s regulatory history, including information regarding whether it was currently involved in any regulatory actions or investigations as well as material litigation.

The Board concluded that the scope and quality of the advisory services provided by VALIC and the Sub-Advisers were satisfactory and that there was a reasonable basis on which to conclude that each would provide a high quality of investment services to the Funds.

Fees and Expenses; Investment Performance. The Board noted that it had received and reviewed total expense information, advisory fee information, and sub-advisory fee information at the 2022 Contracts Review Meeting. The Board also noted that it had received and reviewed information prepared by management and by an independent third-party provider of mutual fund data regarding each Fund’s investment performance compared against its benchmark and performance group and performance universe at the 2022 Contracts Review Meeting. At the 2022 Contracts Review Meeting, the Board had concluded that each Fund’s overall performance was satisfactory in light of the circumstances or was being appropriately addressed by management. The Board also concluded that the advisory fee and sub-advisory fee for each Fund are fair and reasonable in light of the usual and customary charges made for services of the same nature and quality and the other factors considered. In this regard, the Board noted that the same personnel would be providing portfolio management services to each of the Funds.

Cost of Services and Indirect Benefits/Profitability. The Board noted that it had considered profitability to VALIC and the Sub-Advisers at the 2022 Contracts Review Meeting. At the 2022 Contract Review Meeting, the Board also reviewed VALIC’s profitability on a Fund-by-Fund basis, as well as an Investment Management Profitability Analysis prepared by an independent information service, noting that VALIC’s profitability was generally in the range of the profitability of companies contained in the report. The Board also considered that the New Advisory Contracts would not result in any changes to fees. The Board additionally considered that VALIC had represented to the Board that it will use its best efforts to ensure that VALIC and its affiliates do not take any action that imposes an “unfair burden” on the Funds as a result of the Separation Plan or as a result of any express or implied terms, conditions or understandings applicable to a Change in Control Event resulting from the Separation Plan, for so long as the requirements of Section 15(f) of the 1940 Act apply.

Economies of Scale. The Board noted that it had considered economies of scale at the 2022 Contracts Review Meeting. The Board noted that the advisory fee rate and sub-advisory fee rates payable to VALIC and each of the Sub-Advisers with respect to most of the Funds contain breakpoints, which allows the Funds to participate in any economies of scale.

Terms of the Advisory Contracts. The Board reviewed the terms of the New Advisory Contracts including the duties and responsibilities undertaken by the parties. The Board also reviewed the terms of payment for services rendered by VALIC and the Sub-Advisers and noted that VALIC would compensate the Sub-Advisers out of the advisory fees it receives from the Funds. The Board noted that the new sub-advisory agreements provide that each Sub-Adviser will pay all of its own expenses in connection with the performance of their respective duties as well as the cost of maintaining the staff and personnel as necessary for it to perform its obligations. The Board also considered the termination and liability provisions of the New Advisory Contracts and other terms contained therein. The Board additionally considered that the material terms of the Current Advisory Agreement are substantially similar to the material terms of the Proposed Agreement. The Board also considered that the material terms of the Current SunAmerica Sub-Advisory Agreement is substantially similar to the material terms of the New SunAmerica Sub-Advisory Agreement, and noted certain differences in the terms of such Agreements, which are described below under Proposal 3. The Board also considered that the material terms of the current sub-advisory agreements with the unaffiliated Sub-Advisers are substantially similar to the material of the new sub-advisory agreements with the unaffiliated Sub-Advisers. The Board concluded that the terms of each of the New Advisory Contracts were reasonable.

Compliance. The Board noted that it had reviewed VALIC’s and the Sub-Advisers’ compliance personnel and regulatory history, including information on whether they were currently involved in any regulatory actions or investigations in connection with the 2022 Contracts Review Meeting and had concluded that there was no information provided that would have a material adverse effect on their abilities to provide services to the Funds.

Conclusions. In reaching its decision to approve the New Advisory Contracts, the Board did not identify any single factor as being controlling, but based its recommendation on all of the factors it considered.

Each Director may have contributed different weight to the various factors. Based upon the materials reviewed, the representations made and the considerations described above, and as part of their deliberations, the Board, including the Independent Directors, concluded that VALIC and each Sub-Adviser possess the capability and resources to perform the duties required of them under their respective New Advisory Contracts.

Further, based upon its review of the New Advisory Contracts, the materials provided, and the considerations described above, the Board, including the Independent Directors, concluded that (1) the terms of the New Advisory Contracts are reasonable, fair and in the best interests of each Fund and its respective shareholders, and (2) the fee rates payable under the New Advisory Contracts are fair and reasonable in light of the usual and customary charges made for services of the same nature and quality.

Section 15(f) of the 1940 Act

Section 15(f) of the 1940 Act is a non-exclusive safe harbor that provides in substance that, when a sale of a controlling interest in an investment adviser occurs, the investment adviser or any of its affiliated persons may receive any amount or benefit in connection with the sale as long as two conditions are met. If either condition of Section 15(f) is not met, the safe harbor is not available. The first condition specifies that, during the three-year period immediately following consummation of the transaction, at least 75% of the investment company’s board of directors/trustees must not be “interested persons” (as defined in the 1940 Act) of the investment adviser or predecessor adviser. During the three-year period immediately following the consummation of a Change of Control Event resulting from the Separation Plan, it is anticipated that at least 75% of the Directors will not be “interested persons” (as defined in the 1940 Act) of VALIC. The second condition specifies that no “unfair burden” may be imposed on the investment company as a result of the transaction relating to the sale of the controlling interest in the investment adviser, or any express or implied terms, conditions or understandings applicable thereto. The term “unfair burden,” as defined in the 1940 Act, includes any arrangement, during the two-year period after the transaction occurs, whereby the investment adviser (or predecessor or successor adviser), or any interested person of any such investment adviser, receives or is entitled to receive any compensation, directly or indirectly (i) from any person in connection with the purchase or sale of securities or other property, to, from or on behalf of the investment company (other than bona fide ordinary compensation as principal underwriter for the investment company) or (ii) from the investment company or its security holders for other than bona fide investment advisory or other services. VALIC will not impose or seek to impose any “unfair burden” on the Funds as a result of a Change of Control Event resulting from the Separation Plan.

THE BOARD UNANIMOUSLY RECOMMENDS THAT SHAREHOLDERS OF EACH FUND VOTE “FOR” PROPOSAL 2.

PROPOSAL 3

APPROVAL OF INVESTMENT SUB-ADVISORY AGREEMENTS

SHAREHOLDERS OF THE DYNAMIC ALLOCATION FUND, MID CAP INDEX FUND, NASDAQ-100® INDEX FUND, SMALL CAP INDEX FUND, STOCK INDEX FUND, GROWTH FUND, INTERNATIONAL EQUITIES INDEX FUND, INTERNATIONALLY SOCIALLY RESPONSIBLE FUND AND U.S. SOCIALLY RESPONSIBLE FUND (PREVIOUSLY DEFINED AS THE “SUNAMERICA-ADVISED FUNDS”) VOTING SEPARATELY WITH RESPECT TO THEIR FUND

Background